Corporate Asset and Liability Management

Patrocinadora: Petrobras

![]()

Resumo:

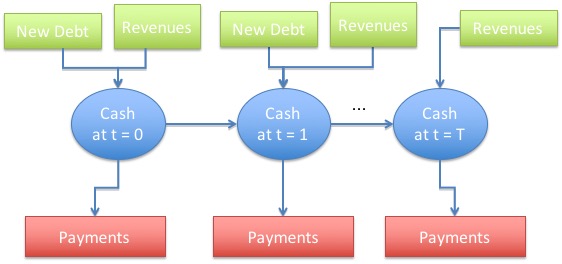

Large corporations fund their capital and operational expenses by issuing bonds with a variety of indexations, denominations, maturities and amortization schedules. In this project we propose, develop and deploy a multistage linear stochastic programming model that optimizes bond issuance by minimizing the mean funding cost while keeping leverage under control and insolvency risk at an acceptable level. The funding requirements are determined by a fixed investment schedule with uncertain cash flows. Candidate bonds are described in a detailed and realistic manner. A specific scenario tree structure guarantees computational tractability even for long horizon problems. We also develop two additional modules, namely, a stochastic model for oil and by-product prices and a stochastic model for interest and exchange rates. Based on the proposed model, a financial planning tool has been implemented and deployed for Brazilian oil company Petrobras.